By Deborah Goonan, Independent American Communities deborahgoonan@gmail.com

Just before the Christmas holiday season, both Fannie Mae and Freddie Mac issued new “temporary guidance” for sellers of units in condominium and cooperative housing projects in the U.S.

On behalf of any buyer that’s planning to make a mortgage purchase of a unit, all condominium and cooperative HOAs must now disclose major deficiencies in the community, as well as any current or pending special assessments intended to pay for major repair and reconstruction.

That guidance could be a game changer in the market for condos and co-ops. To put it bluntly, if a condominium or cooperative structure with 5 or more units is in need of “critical repair,” neither Fannie nor Freddie will purchase unit-owner/shareholder mortgages.

Common sense analysis follows. If Fannie and Freddie won’t buy your mortgage, your lender probably won’t underwrite the loan. If you still want to invest in a unit in a distressed condominium or cooperative project, you’ll probably have to accept less favorable loan terms, or make an all-cash purchase.

In 2020, Bankrate.com reports that Fannie and Freddie owned 62 percent of conforming mortgage loans.

It’s important to note that, according to Freddie Mac’s recent public notice, the new temporary requirements are in direct response to the sudden collapse of Champlain Towers South Condominium, of Surfside, FL, in June of 2021.

The cause or causes of that horrific collapse are currently under investigation, but experts generally agree that a combination of shoddy construction and decades of deferred maintenance led to the demise of the 13-story residential structure, and the death of 98 residents. (In case you’ve been hibernating for the past 7 months, you can read the backstory on Champlain Towers South here on IAC.)

What Critical Repairs must be disclosed by sellers of condos and co-ops?

Let’s take a closer look at Freddie Mac’s form 476, revised December 2021, as well as Bulletin 2021-38, Temporary Condominium and Cooperative Project Requirements and Topic 5600 Reorganization, Issued 12/15/2021.

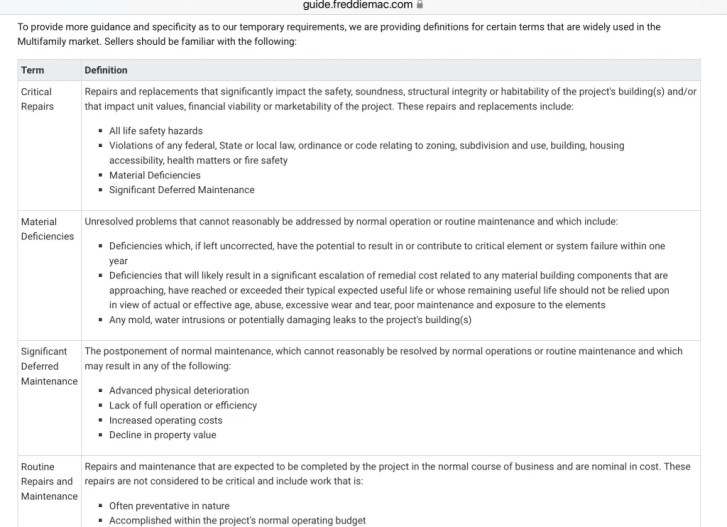

The following screen capture (Jan. 9, 2022), includes the official definition of Critical Repairs that must be disclosed by sellers, which includes HOAs governing 5 or more multifamily units.

As you’ll note, Critical Repairs include Material Deficiencies and Significant Deferred Maintenance, as also defined in Bulletin 2021-38.

For example, any of the following health and safety hazards must be disclosed, in order to obtain a mortgage that the lender plans to sell to Freddie Mac.

Structural defects or deterioration of the building, including balconies and parking garages; non-working fire alarms or fire suppression systems; non-working elevators; lack of adequate heat or air conditioning in the building; recurrent water quality violations for the community’s water supply (well or private utility); collapsed wastewater (sewage) lines; plumbing leaks and resulting mold contamination; extensive damage due to termites, rats, or other pest infestations; leaky roofs, windows, doors, or any portion of the building envelope; deterioration of community-owned access roads and bridges, subject to local code violations.

This is not an exhaustive list, but certainly covers the most common deficiencies that occur in older or poorly-maintained condominiums and cooperatives.

Fannie Mae has also added similar requirements for seller disclosures.

‘Critical Repair’ Disclosures could help home buyers

On a positive note, Fannie and Freddie’s new seller disclosure requirements ought to prevent buyers who plan to mortgage their unit from buying a Lemon that’s going to require huge special assessments and extensive, possibly disruptive construction work to bring the community’s infrastructure up to reasonable health and safety standards.

For the first time in 50 years, a condo or co-op buyer will be more fully informed about both the structural and fiscal integrity of the community association. It’s about time!

Just as the buyer of a single family home would negotiate a lower purchase price — or walk away — following home inspections, a condo or co-op buyer can now exercise similar due diligence by carefully reviewing HOA seller disclosure forms. Obviously, the property value of a unit in a well-maintained community is going to be significantly higher than the value of a unit in a community with a lot of deferred maintenance, big special assessments, and high delinquency rates.

Among unit owners in properties with deferred maintenance, there will be winners and losers

But what if you’re a current unit owner in a condominium or cooperative housing project where Fannie and Freddie won’t back mortgage loans, including refinance loans?

Unfortunately, it’s not good news for owner-occupants, year-round or seasonal owners on fixed incomes, or owners who rely on rental income to supplement their retirement. If you can’t afford to pay the hefty HOA special assessments, and you can’t borrow against your equity, your only option will be to sell your unit to a cash-buying investor. Under the circumstances, investors are likely to make lowball offers, knowing they’ll have to sink a lot of money into the community to turn their investment into a profitable one.

However, Fannie and Freddie’s reluctance to support the riskier side of condo and co-op market is good news for bulk and institutional investors. These folks are always on the hunt for distressed community associations, where they can pick up multiple housing units for pennies on the dollar.

With home purchase prices now out of reach for millions of Americans, and with rental housing in short supply and high demand, the vast majority of multifamily properties are best used as rental homes and apartments.

For that reason, I think it’s likely that 2022 will be a record-breaking year for condominium and cooperative terminations and conversions to traditional commercial rental properties. Communities that are beyond repair are likely on the fast road to condemnation and evacuation of remaining residents.

And there’s no telling how ‘temporary’ these new disclosure requirements will be.

Small community associations, detached condos, exempt from ‘critical repair’ disclosure requirements

Curiously, under Freddie Mac’s current guidance, multifamily community associations with 4 units or less, and detached homes in site condominiums, are not required to disclose critical repairs and special assessments to home buyers. Why these exemptions?

Perhaps detached condominium homes are seen as less risky than multistory buildings with shared walls and foundations. And, obviously, these new disclosure requirements also do not apply to HOA-governed homes in planned communities, presumably for the same reason.

However, homeowners in a growing number of more mature planned communities are now grappling with how to fix their crumbling private roads, how to rebuild structurally unsound private dams for their community lakes, and how to repair or replace shared wells or onsite wastewater treatment systems. It’s not a stretch to assume that, in the near future, Fannie and Freddie will also shy away from backing loans in dysfunctional or distressed planned communities of stand alone homes, too.

As for multifamily condos with 2 to 4 units, the vast majority of these are likely to end up being owned by a singe person or corporate landlord, especially with the current nationwide trend toward relaxing zoning laws to allow for more duplex, triplex, and quadraplex housing (aka ‘missing middle housing’). The movement comes at a time when the U.S. is seeking to increase the supply of affordable housing, while also reversing historically racist zoning practices that limited housing options in many neighborhoods to single family detached homes.

Due to recent legislative reform, developers and private homeowners in California, Oregon, and cities like Minneapolis and Seattle, now have options — and higher economic incentives — to purchase single family homes in need of repair, and convert them to 2, 3, or 4 unit properties. And I have a strong hunch these new owners won’t be converting single family properties to sell them as condominiums. On the contrary, they will be converting them to either rental properties or multigenerational homes.

Apartments and rental homes are replacing HOA-governed condominiums and cooperatives

In conclusion, it appears that the collapse of Champlain Towers South Condominium has accelerated the process of eliminating poorly-managed multifamily condo and co-op community associations, in favor of establishing apartment rental communities.

At the same time, the combination of Fannie Mae’s and Freddie Mac’s temporary lending standards, and the growing trend toward less exclusionary local zoning, may be facilitating a potentially meaningful increase in the supply of more affordable rental homes and multigenerational housing for people who are unable to buy a home, as well as Americans who simply choose not to be homeowners.

News Sources:

After Surfside, a major national condo reform is quietly going into effect WLRN 91.3 FM | By Daniel Rivero. Published January 6, 2022 at 6:12 PM EST

Freddie Mac Establishes Temporary Review Requirements for Certain Condominium and Cooperative Share Projects. TENA, December 20, 2021

Share this:

Discover more from Independent American Communities

Subscribe to get the latest posts sent to your email.

You must be logged in to post a comment.